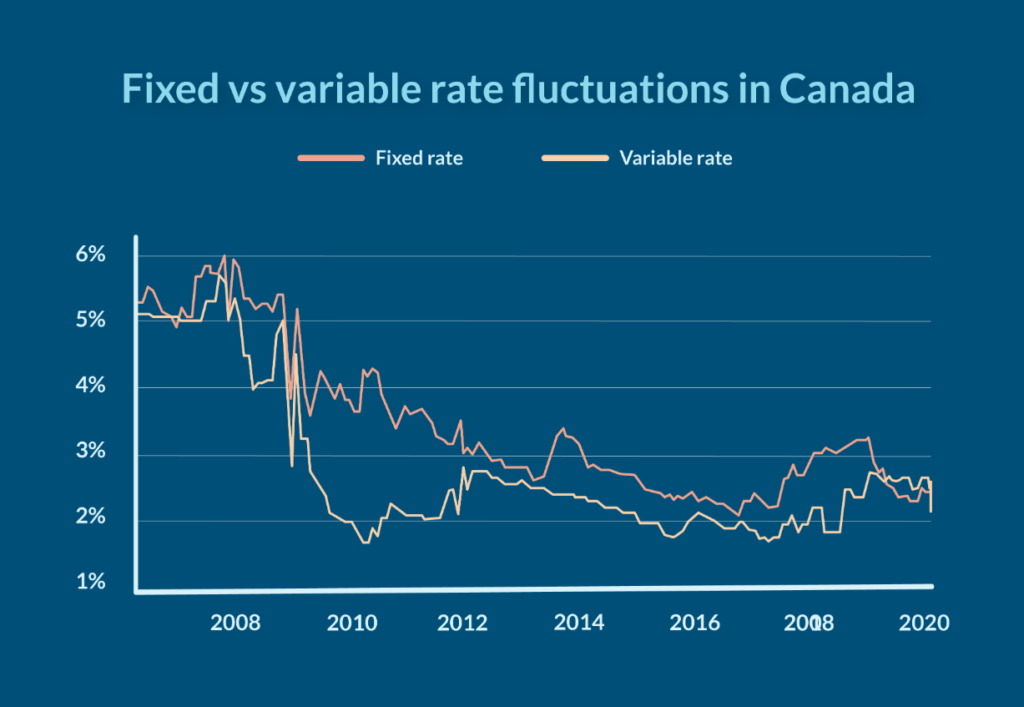

Fixed Rate Mortgage vs Variable Canada: In Canada, a fixed-rate mortgage offers consistent monthly payments with an unchanging interest rate throughout the term. On the other hand, a variable-rate mortgage fluctuates based on the prime lending rate set by your lender, potentially resulting in lower initial rates but higher risk.

Navigating the Canadian mortgage landscape can be daunting, especially when it comes to choosing between fixed and variable rate mortgages. Both offer distinct advantages and disadvantages, and the ‘best’ option depends entirely on your individual financial situation and risk tolerance. Here’s a comprehensive guide to help you make an informed decision.

What is Fixed Rate Mortgage?

A fixed-rate mortgage (FRM) is a type of home loan offered in Canada where the interest rate is locked in for the entire term of the mortgage. This means, unlike a variable-rate mortgage, the interest rate you agree to at the beginning won’t fluctuate with market conditions or changes in the prime rate set by the Bank of Canada.

Key Features:

- Predictable Payments: Your monthly payment remains the same throughout the entire mortgage term, making budgeting and financial planning much easier.

- Stability: You’re protected from rising interest rates. This provides peace of mind, especially during periods of economic uncertainty when interest rates might climb.

- Interest Rate Options: Fixed-rate mortgages come in various terms, typically ranging from 5 to 30 years. The term you choose will affect your interest rate – shorter terms often come with lower rates compared to longer terms.

What is Variable Canada?

A variable-rate mortgage in Canada is a type of home loan where the interest rate fluctuates based on market conditions. Unlike a fixed-rate mortgage, which maintains a consistent interest rate throughout the term, a variable-rate mortgage is tied to the prime rate set by the lender. As the prime rate changes, so does the interest charged on the mortgage. Borrowers with variable-rate mortgages may benefit from lower rates during periods of economic stability. But they also face the risk of higher rates if the prime rate increases. It’s essential for borrowers to assess their risk tolerance and consult with mortgage professionals before choosing between fixed and variable options.

Key Difference

| Aspect | Fixed-Rate Mortgage | Variable-Rate Mortgage |

|---|---|---|

| Interest Rate | Remains constant throughout the term | Changes with the prime lending rate set by your lender |

| Payment Consistency | Stable monthly payments | Payments may fluctuate based on rate changes |

| Risk Tolerance | Low risk, predictable | Higher risk due to potential rate fluctuations |

| Market Trends | Historically popular | Popularity varies based on current rates |

| Lender Relationship | Fixed relationship to prime | Prime +/- a specified amount (e.g., Prime – 0.45%) |

Fixed vs Variable Mortgage in 2024: Which is Right for You?

Choosing between a fixed or variable rate mortgage in Canada depends on your risk tolerance and financial goals in 2024. Fixed rates offer peace of mind with stable monthly payments throughout the term. But can be currently higher than variable rates. Variable rates can potentially save you money if they stay low or decrease, but also expose you to the risk of increases that could strain your budget. Consider your comfort level with payment fluctuations and research interest rate forecasts to make an informed decision. Consulting a mortgage broker can help you assess your situation and choose the best option for your financial security.

Remember

There’s no one-size-fits-all solution. Carefully weigh the pros and cons of fixed and variable rates, considering your personal circumstances and financial goals. Making an informed decision can help you secure a mortgage that aligns with your needs and provides financial stability for the long term.